The EU has a 2030 greenhouse gas (GHG) reduction target of 55% below 1990 levels, in preparation for net-zero GHG emissions in 2050. Regulation (EU) 2021/1119 Article 4(3) of the European Climate Law requires an intermediate 2040 climate target to set the pace for EU-wide reductions of net GHG emissions. The EU Commission unveiled the legislative proposal for this target in early July, and in line with earlier communications and assessment documents, the proposal sets out the binding Union 2040 climate target as a reduction of net GHG emissions (emissions after deduction of removals) by 90% compared to 1990 levels by 2040. But can this be achieved in 15 years?

A recent overview of EU GHG emissions is shown in the table below, extracted from the European Environment Agency GHG database. Only carbon dioxide (CO2), methane (CH4) and nitrous oxide (N2O) are shown.

Greenhouse gas1990 CO2eq Gt2023 CO2eq Gt2023 CO2eq as a % of total 1990 GHG emissionsCO23.772.5152%CH40.670.408.4%N2O0.300.183.8%

Of the 0.58 Gt CO2eq which is CH4 and N2O in 2023, 0.46 Gt comes from agriculture and waste handling, which represent among the most challenging emission reduction tasks. For example, raising cattle means there will be methane emissions – it’s part of bovine biology. Some further reductions in these gases may be possible by optimizing fertilizer use and adjusting cattle feed, but a 90% reduction is unlikely. As such, the non-CO2 greenhouse gases will take a disproportionate part of the remaining 10% of the emissions in 2040, leaving little room for any CO2.

While the 90% GHG reduction by 2040 is not a full transition to net-zero, it nevertheless represents an almost complete transformation of the energy system, because the remaining 10% will be CH4 and N2O emissions from agriculture and some other industrial process GHG emissions (such as fluorinated gases). In such a situation, any remaining fossil fuel CO2 emissions would only be coming from rapidly diminishing legacy uses e.g. some old trucks, a last remaining coal steel mill and so on. In effect, the proposed European target implies net-zero (or nearly net-zero) CO2 emissions in just 15 years.

This means that achieving the 2040 target requires the rapid maturing and full implementation of all available clean energy technologies, not just solar PV and wind, but even nascent technologies such as synthetic aviation fuel (e-SAF) and direct air capture of CO2. And this could be where a problem lies.

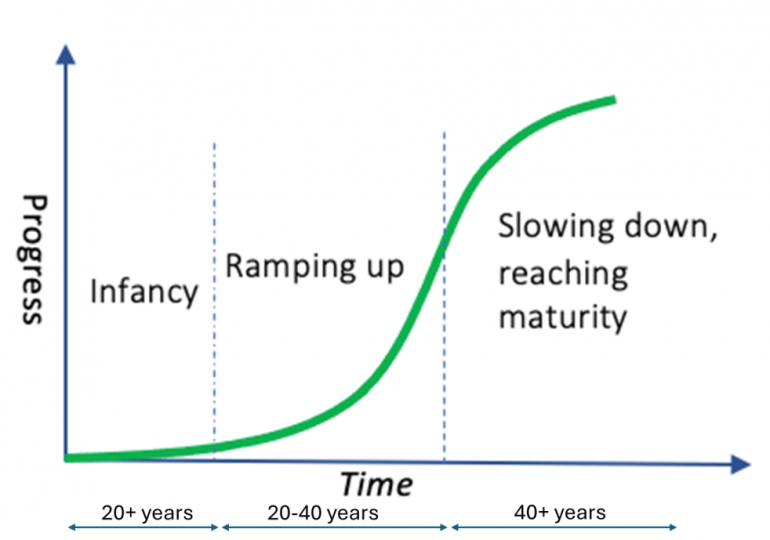

The energy system, like any other advanced technology system, needs to go through phases of implementation in its development. New technologies will enter and establish themselves, after which they will ramp up as costs come down and broad market access is achieved, then finally they will reach a level of market saturation and further growth will be limited. This happens in all markets and takes time. In the energy system the path to full maturity is measured in decades as shown in the illustration. By contrast, in the information technology sector (e.g. smart phones), the timeline is about half that for energy.

The development of solar PV is a good example. Even though the first patent for a solar PV device can be traced back to 1935, the first commercial use of solar PV was by NASA in the 1970s as an expensive but necessary means of powering orbital vehicles like Skylab. The first terrestrial power plant was a 1 MW facility in California, built by the oil company ARCo in 1982. Forty-three years later solar PV generates 13% of global electricity, but most of this has occurred in the last decade.

Looking at the wide range of technologies which we currently use for energy or will use in the years to come, the development curve can be populated as shown. At the far left just entering the mix are technologies like small modular nuclear reactors (SMR) and in the top right corner are mature departing (at least in Europe) technologies like coal fired power stations. Solar PV and wind are now in the fastest part of the ramping up zone.

To date, the transition in Europe has largely relied on wind and solar PV, although more recently passenger electric vehicles (EV) have entered the mainstream. While these three technologies have further to run and can continue to reduce EU emissions, a good portion of remaining emissions won’t be directly reduced by solar PV and wind, other technologies will need to scale up.

In 2025 EU energy system emissions are at about 2.6 Gt CO2, of which 0.6 Gt CO2 is from electricity generation. The remaining 2 Gt is from direct fuel use in road transport, aviation, home heating, cooking and industry. These activities will need to migrate to low carbon fuels like hydrogen or biofuel, be electrified or have their CO2 captured and stored. The issue that Europe faces is that all the technologies required for this 2 Gt are on the left-hand side of the diagram, with several on the far left in their infancy. Some technologies, like EVs, are on the cusp of rapid ramp up, but one technology that is mandated for 2030, notably e-SAF, is arguably still newborn. The 1% mandate for 2030 (and rising to 5% by 2035) will require an initial 10,000 barrels per day of production across the EU.

Although it is clear that an array of relatively new or very new technologies are now required to largely eliminate fossil fuel use or capture CO2 emissions, Europe has nevertheless chosen a 2040 target that front-loads the task into the first 15 years of the next 25 years (to net-zero emissions in 2050), rather than back-loading the task to allow the required technologies to mature.

Front-loading, given ongoing emissions from agriculture, puts significant pressure on hard to abate sectors such as industry and aviation which will need to fully decarbonise by 2040, just 15 years from now.

One way out of this dilemma is to allow the use of a variety of carbon removal offsets into the equation. For example, importing CO2 removal credits from reforestation projects in Brazil under Article 6 of the Paris Agreement could make additional room within the EU carbon budget. This could be both a long-term strategy for the EU or a shorter-term gap-filling measure. The proposed legislation recognizes this in Recital 8.

A number of elements to facilitate the achievement of the 2040 target should be appropriately reflected, including a potential limited contribution towards the 2040 target of high quality international credits under Article 6 of the Paris Agreement, in the second part of the 2030-2040 decade, in line with accounting rules of the Paris Agreement; the role of domestic permanent removals (Biogenic emissions Capture with Carbon Storage (BioCCS) and Direct Air Capture with Carbon Storage (DACCS)) in the EU ETS; enhanced flexibility across sectors.

However, the legislative proposal has also proposed severe constraints on the use of such credits, with a 3% (of 1990 emissions) limit on the use of Article 6 credits and the notion of somehow linking the use of DACCS and BioCCS to residual emissions from hard to abate sectors. Article 4.4 a+b.

Starting from 2036, a possible limited contribution towards the 2040 target of high-quality international credits under Article 6 of the Paris Agreement of 3% of 1990 EU net emissions supporting the EU and third countries in achieving net greenhouse gas reduction trajectories compatible with the Paris Agreement objective to hold the increase in the global average temperature to well below 2°C and pursue efforts to limit the temperature increase to 1.5 °C above pre-industrial levels – the origin, quality criteria and other conditions concerning the acquisition and use of any such credits shall be regulated in Union law;

The role of domestic permanent removals under the greenhouse gas emission allowance trading system within the Union (‘EU ETS’) to compensate for residual emissions from hard to abate sectors;

The use of Article 6, at least over the period 2030 to say 2060, could be a game-changer for the EU and for the host countries receiving investment. The 3% limit needs to be increased considerably.

Both DACCS and BioCCS are also on the left side of the development curve. While there are many small (<10 kt per year CO2) DACCS facilities in operation globally, there is just one large-scale demonstration project in the USA and no large-scale activity at all in Europe, despite some key companies in the DACCS world being based in Europe. The focus on the USA is because of the specific incentives for DACCS within US energy legislation, which also don’t exist in Europe (at least not directly, but there could be support via the EU innovation fund, although no such projects appear on the current funding list). The EU needs to turbo-charge DACCS development over the next decade. It’s also a foundation technology for e-SAF, which is another important element within the EU climate programme, given the mandates for aviation fuel.

The EU Parliament and Council discussions on this legislation over the coming months should prove interesting. MEPs will need to assess how energy system development pathways align with the ambition of the 2040 target and the tools available to deliver it.

Leave a comment